Pocket Option Broker is your go-to platform for online trading in the financial markets

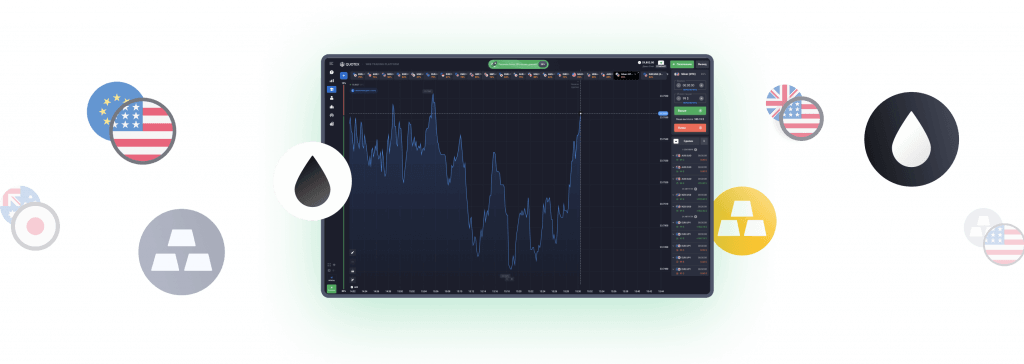

The most user-friendly interface is at your fingertips, granting you access to trade more than 100+ diverse global trading assets.

The most user-friendly interface is at your fingertips, granting you access to trade more than 100+ diverse global trading assets.

We created the most simple and comfortable interface that does not distract from the main thing – from trading

Approach the strategy thoughtfully – the most precise and innovative signals with an accuracy of 87% will help you create your own effective strategy

We have gathered the most useful trading indicators. Use them to boost your account balance

Our platform runs on the most modern technology and delivers incredible speed

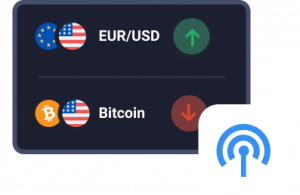

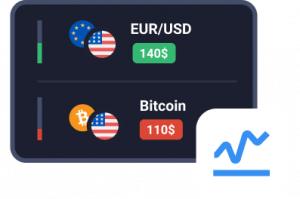

Will the price go Up or Down?

Download our user-friendly application for iPhone or Android and start trading!

Pocket Option Bonus

Start trading and get

30% Bonus on the first deposit

Start trading with a minimum investment of $1. Gain profits without the risk of losing large investments. Available amount of a trade order varies from 1 to 1000 $.

Get a 30% bonus on your first deposit when you make a deposit of $100 or more. Bonus amount can be used for trading and making profits.

Unlimited trading practise on a demo account, with $10 000 on the balance

More than 20 payment methods are available for deposits and withdrawals. Fast transaction processing, platform commission 0%.

You can always get quick-response and around-the-clock support. Create a ticket to get assistance from support service

When replenishing the balance from $1000 You will have access to extra benefits from the raised level in the form of an increased percentage of profitability and advantageous promo codes

Great platform, everything works without problems. The support service is excellent, they always help in controversial situations. Furthermore, the trading platform works at excellent speed, along with online quotes and the ability to set an expiration from 1 minute to 4 hours.

Deemitrus

ID: 77455662

What a wonderful operation. Excellent app for trading. Always withdraws early. It does not manipulate like other platform apps. I am using this app since the beginning and it is a very good app. Customer service is excellent. They give all the answers and solve all the questions in no time. I recommend using this app for trading. Very good in all aspects. No app can compete with this one. All indicators in the app are easy to use. Anyone can use these indicators with ease. Amazing app to operate.

Deemitrus

ID: 77455662

Quotex is really a good platform for trading. The charts are fast in terms of response to market fluctuations and highly customizable. The platform has dozens of the most common indicators, each of which can be precisely adjusted to the personal taste of each trader. Deposits and withdrawals are also very fast.

ashok kumar

ID: 123332164

Open an account for free in just a few minutes

Get your skills better with a demo account and training materials

Over 410 instruments and a minimum deposit of $5 for optimal trading

Use a wide range of indicators for strategies and market analysis and increase your chances of successful trades

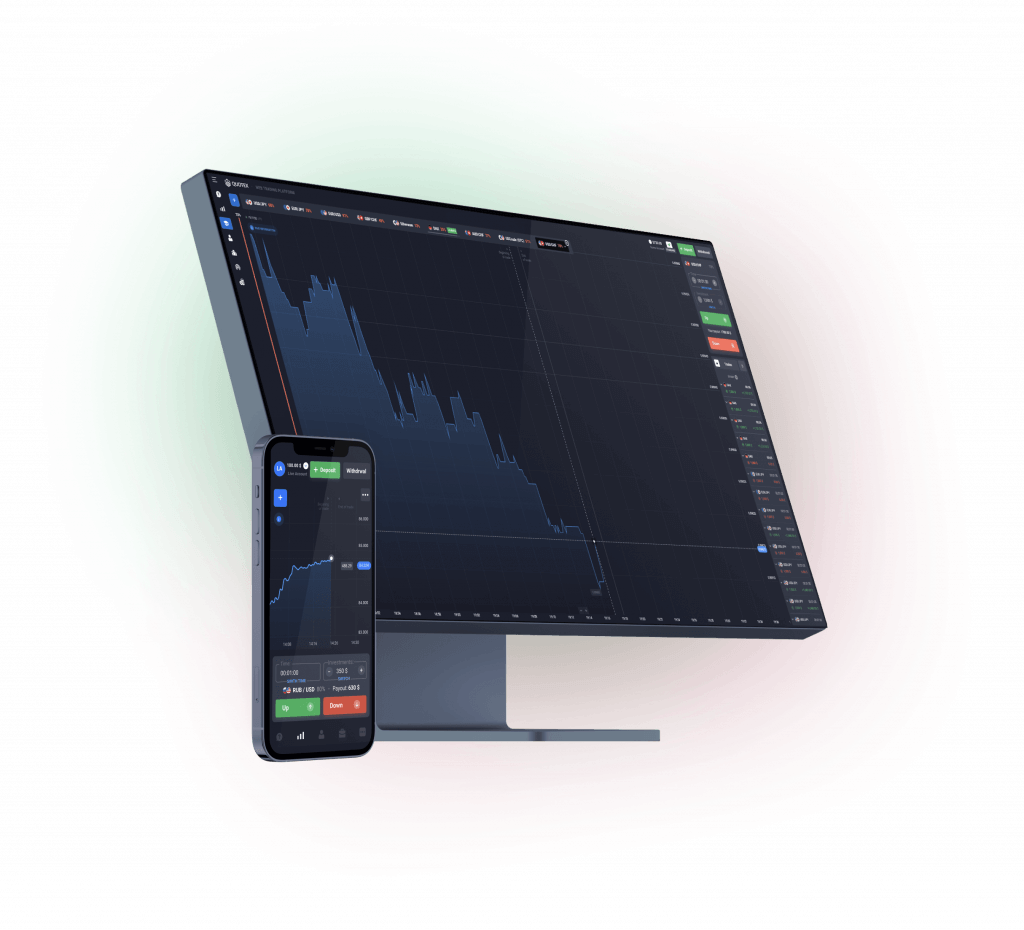

Trade whenever and wherever it is convenient using a laptop or smartphone

Minimum deposit and withdrawal amount - $10 no fees

Simple and intuitive interface with convenient settings

Close the deal at any time

Trade and watch your position in the ranking, among other traders from all over the world

Sign up Pocket Trading and train on a demo account. It is exactly the same as real trading, but for free.

On average, the withdrawal procedure takes from one to five days from the date of receipt of the corresponding request of the Client and depends only on the volume of simultaneously processed requests. The company always tries to make payments directly on the day the request is received from the Client.

Trading platform – a software complex that allows the Client to conduct trades (operations) using different financial instruments. It has also accesses to various information such as the value of quotations, real-time market positions, actions of the Company, etc.

Our platform runs on the most modern technology and opens in the browser of any computer or mobile phone

The advantage of the Company’s trading platform is that you don’t have to deposit large amounts to your account. You can start trading by investing a small amount of money. The minimum deposit is 10 US dollars.

No. The company does not charge any fee for either the deposit or for the withdrawal operations.

However, it is worth considering that payment systems can charge their fee and use the internal currency conversion rate.